If you’ve ever bought Bitcoin or Ethereum, you’ve probably experienced the stomach-churning sensation of watching your investment swing 20% in a single day. Now imagine a cryptocurrency that doesn’t do that – one that stays reliably pegged to $1, combining the benefits of blockchain technology with the stability of traditional money. That’s exactly what stablecoins are designed to do.

Stablecoins are cryptocurrencies engineered to maintain a stable value, typically pegged to the US dollar at a 1:1 ratio. Unlike volatile cryptocurrencies such as Bitcoin or Ethereum, stablecoins like USDC, USDT, and DAI aim to always equal one dollar. Consequently, they provide the speed, transparency, and global accessibility of blockchain without the price rollercoaster that makes traditional crypto unsuitable for everyday transactions.

In this comprehensive guide, I’ll draw on my decade of experience teaching cryptocurrency fundamentals to explain exactly how stablecoins work, compare the major types, share critical lessons from spectacular failures like Terra/UST, and help you understand when and why you might actually use them.

Table of Content

- The Problem Stablecoins Solve: Why Crypto Needed Stability

- What Are Stablecoins and How Do They Maintain Value?

- The 4 Types of Stablecoins Explained (With Examples)

- How Do Fiat-Backed Stablecoins Work? (USDC & USDT Deep Dive)

- Understanding Crypto-Collateralized Stablecoins (DAI Explained)

- Why Stablecoins Matter: 5 Real-World Use Cases

- Stablecoin Risks You Must Know (Depeg, Regulation & More)

- How to Choose the Best Stablecoin for Your Needs

- The Future of Stablecoins: CBDCs, Regulation & Mass Adoption

- Are Stablecoins Safe? Common Questions Answered

- Final Thoughts: Using Stablecoins Wisely in 2025

- About This Guide

- References

The Problem Stablecoins Solve: Why Crypto Needed Stability

Bitcoin launched in 2009 with a revolutionary promise: decentralized, borderless digital money. However, early adopters quickly discovered a fundamental problem. How can something be used as money when its value swings wildly from day to day?

Imagine trying to buy coffee with Bitcoin. You’d need to check the price every few minutes because your $5 coffee might cost $6 by the time you reach the counter. Furthermore, merchants couldn’t price their goods in Bitcoin because they’d lose money if the price dropped before they converted it to dollars.

This volatility problem created several major headaches:

Payment Uncertainty: Businesses couldn’t accept crypto for goods and services when the value fluctuated unpredictably. A $100 sale might be worth $85 or $115 by the end of the day.

Trading Friction: Crypto traders needed a way to exit positions quickly without converting back to traditional bank accounts, which could take days. Moreover, moving money on and off exchanges incurred fees and regulatory scrutiny.

Lost Opportunities: International remittances, cross-border business payments, and access to stable currency for people in high-inflation countries all remained difficult. Traditional crypto was too volatile to serve these vital use cases.

Stablecoins emerged as the solution to these problems. By maintaining a stable $1 value, they enable practical blockchain applications while preserving the core benefits of cryptocurrency: 24/7 global transfers, transparency, programmability, and independence from traditional banking infrastructure.

What Are Stablecoins and How Do They Maintain Value?

At their core, stablecoins are cryptocurrencies with a stability mechanism. While Bitcoin’s price is determined purely by market forces, stablecoins use various methods to maintain their $1 peg.

Think of stablecoins like a coat check system. You hand over your coat (deposit $1), receive a ticket (get 1 stablecoin), and can later return the ticket to reclaim your coat (redeem for $1). The ticket itself might change hands multiple times, but it always represents one coat in storage.

Different stablecoins use different “coat check” systems:

Fiat-backed stablecoins hold actual dollars in bank accounts or safe investments. For every token in circulation, there’s supposedly a dollar sitting in reserve. This is the most straightforward approach and powers the largest stablecoins like USDC and USDT.

Crypto-backed stablecoins use other cryptocurrencies as collateral, typically locked in smart contracts. Because crypto is volatile, these stablecoins require over-collateralization – you might need to lock up $150 of Ethereum to mint $100 worth of stablecoins.

Algorithmic stablecoins attempt to maintain stability through supply-and-demand mechanisms without direct backing. As we’ll discuss, this approach has proven extremely risky, with the catastrophic $40 billion collapse of Terra/UST in May 2022 serving as a stark warning.

Commodity-backed stablecoins are pegged to physical assets like gold rather than dollars. Each token represents ownership of a specific amount of the underlying commodity.

The stability mechanism matters enormously because it determines the stablecoin’s safety, decentralization level, and risk profile. Understanding these differences is crucial for making informed decisions about which stablecoins to trust.

The 4 Types of Stablecoins Explained (With Examples)

Let’s dive deeper into each stablecoin category. Each type has distinct advantages, risks, and ideal use cases.

What Are Fiat-Collateralized Stablecoins?

Fiat-collateralized stablecoins are the most popular and easiest to understand. They work exactly like the coat check analogy: real dollars back each token.

For every USDC token in circulation, Circle (the issuer) holds $1 in reserves. These reserves typically consist of cash in bank accounts and short-term U.S. Treasury bills – extremely safe, liquid assets. Similarly, Tether holds reserves to back every USDT token, though the composition of these reserves has historically been less transparent.

The appeal is straightforward. If the stablecoin is properly backed, you can always redeem it for $1. This creates a natural price floor – if USDC trades below $1 on exchanges, arbitrageurs buy it cheap and redeem it for the full dollar, pocketing the difference. Conversely, if it trades above $1, they can mint new tokens for $1 and sell them at a premium.

Major fiat-backed stablecoins include:

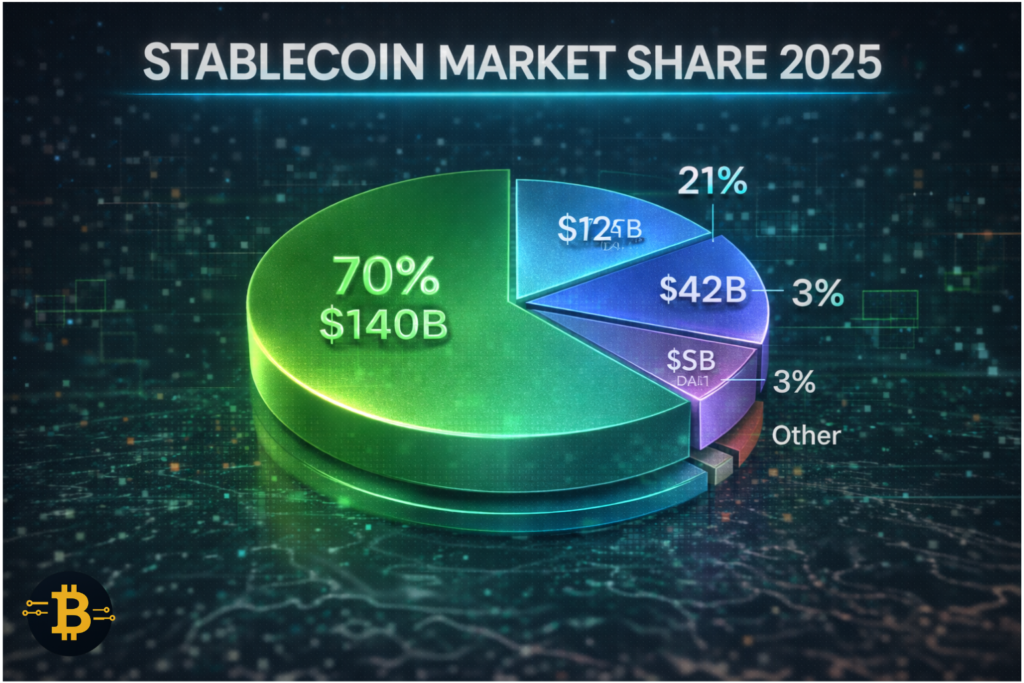

- USDC (USD Coin) – Issued by Circle, ~$42 billion market cap

- USDT (Tether) – Largest stablecoin, ~$140 billion market cap

- PYUSD (PayPal USD) – Issued by PayPal, growing rapidly

- BUSD (Binance USD) – Previously major, now being phased out

The main risks involve reserve transparency, regulatory compliance, and the possibility of bank failures affecting the backing assets (as happened briefly with USDC during the Silicon Valley Bank crisis in March 2023).

How Crypto-Backed Stablecoins Maintain Stability

Crypto-collateralized stablecoins take a different approach. Instead of dollars in a bank, they’re backed by other cryptocurrencies locked in blockchain-based smart contracts.

The most prominent example is DAI, created by the MakerDAO protocol. To mint DAI, users deposit cryptocurrencies like Ethereum as collateral. However, because crypto is volatile, the system requires over-collateralization – typically 150% or more.

Here’s how it works in practice:

Let’s say you want to create 1,000 DAI. You’d need to deposit at least $1,500 worth of Ethereum into a MakerDAO vault. Your Ethereum stays locked as long as the DAI exists. If Ethereum’s price drops significantly, the protocol automatically liquidates your collateral to ensure the DAI remains backed.

Think of this like a pawn shop. You bring in your guitar (Ethereum), which might be worth $1,500, and the shop lends you $1,000. If your guitar’s value drops too much, they sell it to recover their money. The difference is that everything happens automatically through smart contracts, with no human decision-maker.

Advantages of crypto-backed stablecoins:

- Fully transparent – all collateral is visible on the blockchain

- No need to trust banks or centralized issuers

- More censorship-resistant than fiat-backed versions

- Truly decentralized when done right

Disadvantages:

- Capital inefficient (requires more than $1 to create $1 worth)

- Complex liquidation mechanisms that can fail during market stress

- Still exposed to crypto market volatility through the collateral

- Smart contract bugs could threaten the entire system

DAI has maintained its peg remarkably well since 2017, though it has experienced brief deviations during extreme market conditions. It represents roughly $5 billion in market cap, making it the largest decentralized stablecoin.

Why Algorithmic Stablecoins Are Controversial

Algorithmic stablecoins attempt the holy grail: maintaining a stable value without backing reserves at all. Instead, they rely on incentive mechanisms and market forces to keep the price at $1.

This approach is theoretically elegant but has proven catastrophically fragile in practice. The story of Terra (LUNA) and its stablecoin UST serves as the definitive cautionary tale.

How Terra/UST Was Supposed to Work:

Terra created a dual-token system. UST was the stablecoin pegged to $1, while LUNA was a separate token that absorbed volatility. Users could always trade $1 worth of LUNA for 1 UST, or vice versa, through the protocol.

If UST traded below $1, arbitrageurs would buy it cheap, burn it to mint LUNA, and sell the LUNA for profit. This would reduce UST supply and push the price back up. If UST traded above $1, the opposite would happen – people would burn LUNA to mint new UST and sell it for profit, increasing supply and pushing the price down.

For months, this worked. UST grew to become the third-largest stablecoin with over $18 billion in circulation. The Terra ecosystem offered attractive interest rates (up to 20% on UST deposits through the Anchor protocol), drawing billions in investment.

Then it collapsed spectacularly in May 2022.

The Terra/UST Collapse: What Went Wrong

The collapse happened over just a few days in a death spiral that destroyed $40 billion in value. Here’s what happened:

May 7-9, 2022: Large UST holders began withdrawing from Anchor and selling UST. The price depegged from $1 to around $0.98. Normally this would be easily corrected, but market conditions were already fragile.

May 10: Panic selling increased as the peg weakened to $0.90. Crucially, the Luna Foundation Guard tried to defend the peg by selling billions in Bitcoin reserves, but it wasn’t enough. The arbitrage mechanism meant to restore the peg began minting massive amounts of new LUNA tokens.

May 11-12: The death spiral accelerated. More UST redemptions created more LUNA tokens, hyperinflating LUNA’s supply. As LUNA’s price collapsed, confidence in the system evaporated entirely. UST fell below $0.30.

May 13: UST was trading under $0.10 and LUNA had essentially become worthless. What started as a $18 billion stablecoin and a $40 billion ecosystem had collapsed to near zero.

Critical Lessons from the Terra Collapse:

First and foremost, algorithmic stablecoins without collateral are fundamentally unstable during extreme market stress. The mechanism that maintains the peg during normal times can amplify a crisis through reflexive feedback loops.

Additionally, unsustainable yields (like Anchor’s 20% interest) often signal underlying risks rather than genuine value creation. These rates couldn’t last and attracted speculative capital that fled at the first sign of trouble.

Third, even large size doesn’t guarantee safety. Terra was a top-10 cryptocurrency and UST was the third-largest stablecoin, yet it collapsed in days. Market cap alone doesn’t indicate resilience.

Finally, the crypto market learned that not all stablecoins are created equal. Reserve backing matters enormously, and transparency provides critical reassurance during market stress.

Some algorithmic stablecoins still exist, but they’ve largely fallen out of favor. The Terra collapse dealt a devastating blow to the entire category’s credibility.

Commodity-Backed Stablecoins: Digital Gold (PAXG)

Commodity-backed stablecoins offer a different value proposition entirely. Rather than maintaining a $1 peg, they’re pegged to physical assets like gold.

Pax Gold (PAXG) is the leading example. Each PAXG token represents one troy ounce of physical gold stored in professional vaults. The current price tracks gold’s market value rather than staying at $1.

This serves a different purpose than dollar-pegged stablecoins. PAXG provides:

Inflation Protection: Gold historically preserves purchasing power over long periods, unlike fiat currencies. Therefore, holding PAXG can serve as a hedge against dollar devaluation.

Easy Trading: Instead of dealing with the logistics of buying, storing, and securing physical gold, you can trade PAXG instantly on crypto exchanges. Moreover, you can hold fractional amounts (0.1 PAXG) rather than buying whole bars.

Blockchain Benefits: You can transfer PAXG globally in minutes, use it in DeFi protocols, or hold it in a self-custody wallet. These features aren’t possible with traditional gold investments.

Verifiable Backing: Paxos, the issuer, provides monthly attestations from independent auditors verifying that physical gold backs the tokens. This transparency exceeds what’s typical in traditional gold investment products.

However, commodity-backed stablecoins come with unique considerations:

The price fluctuates with the underlying commodity rather than staying stable. PAXG isn’t useful for payments or as a stable store of value in the short term—it’s an investment vehicle.

Storage and redemption fees apply. If you want to redeem PAXG for physical gold, minimum redemption amounts and fees make this practical only for larger holdings.

Regulatory complexity increases because these tokens represent ownership claims on physical assets. Different jurisdictions treat them differently for tax and legal purposes.

Commodity-backed stablecoins serve investors seeking blockchain-based exposure to traditional assets rather than those needing a stable medium of exchange.

How Do Fiat-Backed Stablecoins Work? (USDC & USDT Deep Dive)

Let’s examine the two largest fiat-backed stablecoins in detail: USDC and USDT. Together, they account for over $180 billion in market capitalization and dominate global stablecoin usage.

How USDC Maintains Its $1 Peg

Circle issues USDC with a straightforward promise: every token is backed by one dollar held in reserve. The company maintains these reserves in two forms:

Cash deposits in regulated U.S. banks account for a portion of reserves. These provide immediate liquidity for redemptions.

U.S. Treasury bills make up the majority of backing. These short-term government debt instruments are considered essentially risk-free and generate modest returns for Circle.

Monthly attestation reports from Grant Thornton, a major accounting firm, verify that reserves equal or exceed circulating USDC. Circle publishes these reports publicly, providing unprecedented transparency for a financial product.

The Minting Process:

When you want to create USDC, you transfer dollars to Circle. The company verifies the transfer and mints an equivalent amount of USDC tokens, which appear in your blockchain wallet. The entire process typically completes within one business day.

The Redemption Process:

Conversely, when you want to convert USDC back to dollars, you send the tokens to Circle through an authorized partner. Circle burns (permanently destroys) the tokens and wires dollars to your bank account. Again, this usually takes one business day.

How the Peg Stays Stable:

On crypto exchanges, USDC might trade slightly above or below $1 due to temporary supply-demand imbalances. However, arbitrageurs quickly correct these deviations.

If USDC trades at $1.01, arbitrageurs can mint new tokens for $1 and immediately sell them for $1.01, pocketing the difference. This increases supply and pushes the price back down.

If USDC trades at $0.99, arbitrageurs buy it cheaply and redeem it with Circle for $1, making a profit. This reduces supply and pushes the price back up.

This arbitrage mechanism keeps USDC tightly pegged to $1 under normal market conditions.

What Backs Tether (USDT)? Reserve Transparency Explained

Tether (USDT) is the world’s largest stablecoin by market cap, with over $140 billion in circulation. It operates on a similar principle to USDC but with significant differences in transparency and reserve composition.

Reserve Composition:

Tether’s reserves are more diverse than USDC’s. According to recent attestations, they include:

- U.S. Treasury bills (majority)

- Cash and bank deposits

- Money market funds

- Corporate bonds and precious metals (smaller portions)

- Secured loans (controversial component)

This diversification potentially offers higher returns for Tether but introduces more risk compared to USDC’s simpler reserve structure.

Transparency Concerns:

Historically, Tether faced serious criticism for lack of transparency. For years, the company provided limited information about reserves, leading to persistent questions about whether USDT was fully backed.

These concerns peaked when investigations revealed that Tether reserves had previously included commercial paper and other less-liquid assets. Additionally, a 2021 settlement with the New York Attorney General revealed that Tether had at times lacked full backing for its tokens.

Recent improvements include:

- Quarterly attestations from BDO Italia (though not full audits)

- Public breakdown of reserve composition

- Movement toward safer, more liquid assets

- Increased regulatory cooperation

Why USDT Remains Dominant:

Despite transparency concerns, USDT maintains the largest market share because of:

Network Effects: It’s been around since 2014 and has become the default trading pair on most exchanges. Consequently, traders continue using it because everyone else does.

Liquidity: USDT has the deepest liquidity pools, meaning you can trade large amounts with minimal price impact. This makes it preferable for institutional traders and market makers.

Global Reach: USDT is available on more blockchains and exchanges than any competitor. It’s often the only stablecoin option in certain markets.

Trading Pairs: Most cryptocurrency trading pairs are denominated in USDT rather than USDC or other stablecoins. Switching would require significant market infrastructure changes.

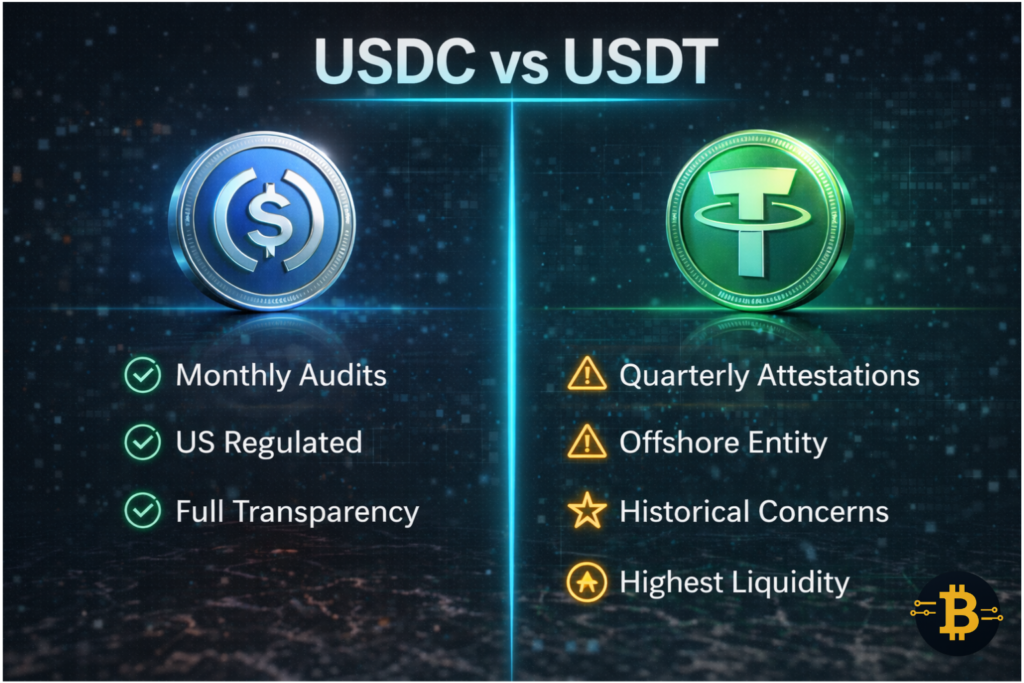

Circle vs Tether: Which Is More Trustworthy?

The USDC versus USDT debate ultimately comes down to transparency versus liquidity.

Choose USDC if you prioritize:

- Regulatory compliance (Circle is a U.S.-regulated company)

- Reserve transparency (monthly attestations, simple composition)

- Institutional acceptance (many institutions prefer USDC)

- Lower perceived risk

Choose USDT if you need:

- Maximum liquidity (deepest order books)

- Widest availability (most exchanges and trading pairs)

- Lowest trading fees (competitive spreads)

- Access to certain markets where USDC isn’t available

Many sophisticated users hold both, using USDC for long-term holdings and USDT for active trading. This strategy balances safety with liquidity.

Importantly, both have maintained their peg effectively over time. USDC briefly depegged to $0.88 during the Silicon Valley Bank crisis in March 2023 but recovered quickly. USDT has generally held its peg even during extreme market stress.

Neither is completely risk-free, but both are dramatically safer than algorithmic stablecoins and have proven resilient through multiple market cycles.

Understanding Crypto-Collateralized Stablecoins (DAI Explained)

DAI represents a fascinating experiment in decentralized stablecoin design. Unlike USDC and USDT, which rely on centralized companies holding bank deposits, DAI is created and managed by smart contracts on the Ethereum blockchain.

How DAI Works: The MakerDAO System

MakerDAO is a decentralized autonomous organization (DAO) that manages the DAI stablecoin through a system of smart contracts called the Maker Protocol.

Creating DAI (Opening a Vault):

Users who want to generate DAI must first deposit cryptocurrency collateral into a Maker Vault. Ethereum is the most common collateral, but the protocol also accepts other cryptocurrencies.

Because crypto values fluctuate, the protocol requires over-collateralization. Typically, you must deposit at least 150% of the value of DAI you want to create. So to generate 1,000 DAI, you’d need to lock up at least $1,500 worth of Ethereum.

Once your collateral is locked, the protocol mints new DAI tokens that you can spend, trade, or invest as you wish. Your collateral remains locked until you return the borrowed DAI.

Maintaining Collateralization:

The protocol constantly monitors the value of your collateral. If Ethereum’s price drops and your collateral ratio falls below the minimum (called the liquidation ratio), the system automatically liquidates your position.

Liquidation works like this: The protocol auctions off your collateral to pay back the DAI debt plus a penalty fee. Therefore, users must actively manage their positions during volatile market conditions.

Smart borrowers maintain healthy margins above the minimum. For example, maintaining a 200% collateral ratio provides a buffer against price swings.

Returning DAI (Closing a Vault):

When you want your collateral back, you simply return the borrowed DAI plus accumulated fees to the protocol. The smart contract then burns the returned DAI and unlocks your collateral.

This creates a natural mechanism for managing DAI supply. When people close vaults, DAI supply decreases. When they open new vaults, supply increases. Market forces and fee structures influence these decisions.

Why DAI Is Different: Decentralization Benefits

DAI’s decentralized nature provides several unique advantages:

No Central Failure Point: There’s no single company that can freeze your funds, go bankrupt, or lose its bank accounts. The entire system runs on smart contracts that execute automatically.

Transparent Collateral: Anyone can verify on the blockchain that sufficient collateral backs every DAI in circulation. You don’t need to trust attestation reports – the data is publicly verifiable in real-time.

Censorship Resistance: Because no central entity controls DAI, it’s much harder for governments or companies to block transfers or freeze funds. This matters greatly for users in countries with capital controls.

Community Governance: MKR token holders vote on system parameters like collateral types, fees, and risk settings. This democratic approach theoretically aligns the system with user interests.

DAI Risks and Considerations

However, DAI isn’t without risks:

Smart Contract Risk: Bugs in the complex system of smart contracts could potentially be exploited. While the Maker Protocol has been extensively audited and has operated securely since 2017, smart contract risks never entirely disappear.

Collateral Volatility: During extreme market crashes, mass liquidations can occur. If liquidations happen faster than the system can process them, DAI could temporarily lose its peg.

Centralization Creep: Interestingly, DAI has become more centralized over time. The protocol now accepts USDC as collateral, meaning a significant portion of DAI is indirectly backed by Circle’s reserves. This improves stability but reduces decentralization.

Complexity: Understanding how DAI works requires more technical knowledge than fiat-backed stablecoins. This complexity can be a barrier for mainstream adoption.

Scalability Limitations: Creating DAI through over-collateralization is capital inefficient. The system can’t scale as easily as simply minting tokens backed by bank deposits.

DAI has successfully maintained its peg through multiple market cycles, including the 2020 crypto crash and the 2022 Terra collapse. It represents approximately $5 billion in market cap, making it the largest decentralized stablecoin and a crucial piece of DeFi infrastructure.

Why Stablecoins Matter: 5 Real-World Use Cases

Beyond theoretical benefits, stablecoins solve real problems for millions of people worldwide. Let’s explore the most important use cases.

Using Stablecoins in High-Inflation Countries

Perhaps the most impactful use case for stablecoins is providing access to stable currency in countries experiencing high inflation.

In Argentina, annual inflation has exceeded 100% in recent years. Savings in pesos lose value rapidly, making it impossible for citizens to preserve wealth. However, strict capital controls prevent most people from accessing U.S. dollars through traditional banking.

Stablecoins offer a workaround. Argentinians can convert pesos to USDT or USDC through peer-to-peer exchanges, gaining exposure to dollar stability without needing international bank accounts. Millions of people across Latin America, Africa, and other regions use stablecoins for this exact purpose.

In Lebanon, the currency collapsed dramatically during economic crisis. The official exchange rate diverged wildly from reality, and banks imposed strict withdrawal limits. Lebanese citizens turned to stablecoins to protect their savings and conduct basic commerce when the traditional financial system failed.

These examples aren’t theoretical. Survey data suggests that over 20% of crypto users in high-inflation countries hold stablecoins primarily as a store of value rather than for trading or speculation.

How Stablecoins Revolutionize Cross-Border Payments

International money transfers through traditional banks are slow, expensive, and opaque. A wire transfer from the U.S. to the Philippines might cost $30-50 in fees, take 2-5 business days, and involve unclear exchange rates.

Stablecoins dramatically improve this experience:

Cost: Transferring USDC costs a few cents on some blockchains (like Solana or Polygon) rather than percentage-based fees. A $1,000 transfer might cost $0.50 instead of $50.

Speed: Stablecoin transfers settle in minutes rather than days. Recipients can access funds almost immediately, which matters enormously for time-sensitive needs.

Transparency: Blockchain transactions are fully visible. Senders and recipients can track transfers in real-time without calling banks or dealing with opaque systems.

Accessibility: You only need a smartphone and internet connection to send or receive stablecoins. No bank account required, which matters for the 1.7 billion adults worldwide who are unbanked.

Remittances represent a massive market – migrant workers send over $600 billion annually to their home countries. Even small reductions in fees can keep billions more dollars in recipients’ pockets rather than going to intermediaries.

Companies like Stellar and Ripple have built entire business models around enabling stablecoin-based cross-border payments. Traditional payment companies like PayPal have launched their own stablecoins partly to compete in this space.

Earning Interest on Stablecoins: DeFi Opportunities

Decentralized finance (DeFi) protocols offer opportunities to earn interest on stablecoin holdings—often at rates significantly higher than traditional savings accounts.

How Stablecoin Yields Work:

DeFi lending protocols like Aave and Compound allow users to deposit stablecoins into liquidity pools. Borrowers can then borrow these stablecoins by posting collateral, paying interest rates set by supply and demand.

For example, you might deposit 10,000 USDC into Aave and earn 4-6% annual interest. This interest accrues continuously and can be withdrawn at any time. Unlike traditional banks, there are no minimum deposit requirements or account fees.

Liquidity Provision:

Alternatively, you can provide stablecoins to decentralized exchanges as liquidity. Traders pay fees to use these liquidity pools, and providers earn a share of those fees.

For instance, providing USDC-ETH liquidity on Uniswap might earn 5-15% annually, depending on trading volume and fee settings.

Important Risks:

However, DeFi yields come with significant risks:

- Smart contract risk: Bugs or exploits could drain funds

- Impermanent loss: For liquidity pairs with volatile assets

- Protocol risk: The DeFi protocol itself could fail or be exploited

- Regulatory risk: Uncertain regulatory treatment of DeFi yields

Yields also fluctuate based on market conditions. Rates that seem attractive during high activity might drop significantly during quiet periods.

Many sophisticated users view DeFi stablecoin yields as a higher-risk alternative to traditional savings, appropriate for a portion of their holdings but not all. Always research protocols thoroughly and never invest more than you can afford to lose.

Stablecoins for Business: Payroll and Payments

Businesses increasingly use stablecoins for operations, especially companies with international teams or customers.

Payroll Benefits:

Companies with remote workers across multiple countries face enormous friction paying salaries. Traditional international payroll requires setting up local entities, dealing with multiple banks, and paying high fees.

Stablecoin payroll simplifies this dramatically. A U.S. company can pay Filipino and Argentinian employees directly in USDC within minutes at minimal cost. Employees receive stable dollar-denominated pay without needing U.S. bank accounts.

Several startups now offer stablecoin payroll services, handling compliance and conversion for both companies and employees. This model is particularly popular in the crypto industry itself but is expanding to other sectors.

B2B Payments:

Business-to-business payments suffer similar problems as consumer remittances. International invoices take days to settle, involve high fees, and create cash flow management headaches.

Stablecoin payments between businesses settle in minutes, with full transparency about when payment arrives. This accelerates business operations and reduces working capital requirements.

Treasury Management:

Some companies now hold a portion of treasury reserves in stablecoins rather than traditional bank accounts. This provides flexibility to access DeFi yields while maintaining dollar stability.

However, accounting and tax treatment remains complex. Companies must carefully consider regulatory implications and work with advisors who understand crypto assets.

Crypto Trading: Why Traders Need Stablecoins

For cryptocurrency traders, stablecoins are absolutely essential infrastructure.

Quick Exits from Volatility:

When market conditions deteriorate, traders need to exit positions quickly. Selling Bitcoin for stablecoins takes seconds on any exchange. Converting Bitcoin to dollars and withdrawing to a bank account takes days.

Therefore, stablecoins function as a safe harbor during market storms. Traders can preserve capital while remaining ready to re-enter positions when opportunities appear.

Trading Pair Liquidity:

Most cryptocurrency trading pairs quote prices in USDT or USDC rather than fiat currencies. Want to trade Solana for Avalanche? You’ll likely trade SOL/USDT and then USDT/AVAX rather than directly swapping.

This creates deep, liquid markets because stablecoins act as universal intermediaries. The same USDT liquidity serves traders interested in hundreds of different cryptocurrencies.

Yield While Waiting:

Rather than keeping dollars in a zero-interest exchange wallet, traders can deploy stablecoins to earn yields while waiting for trading opportunities. This improves capital efficiency significantly.

Arbitrage Trading:

Professional arbitrageurs rely on stablecoins to quickly move value between exchanges and capture pricing differences. The speed and efficiency of stablecoin transfers makes this arbitrage practical.

For professional traders, stablecoins aren’t just useful – they’re indispensable. The cryptocurrency market would function far less efficiently without them.

Stablecoin Risks You Must Know (Depeg, Regulation & More)

While stablecoins offer compelling benefits, they’re far from risk-free. Understanding these risks is crucial for making informed decisions.

What Causes Stablecoin Depegging?

Depegging occurs when a stablecoin’s market price deviates significantly from its intended $1 target. Several factors can cause this:

Bank Failures:

In March 2023, Silicon Valley Bank collapsed. Circle held approximately $3.3 billion of USDC reserves there. When the bank failed, these funds were temporarily frozen, creating uncertainty about whether USDC was fully backed.

USDC’s price dropped to $0.88 as panicked holders sold. The depeg lasted about 72 hours until the U.S. government announced that all SVB deposits would be honored. USDC quickly recovered to $1, but the incident highlighted how fiat-backed stablecoins are exposed to traditional banking system risks.

Liquidity Crises:

During extreme market volatility, stablecoins can temporarily depeg due to liquidity imbalances. If millions of people try to sell simultaneously and not enough buyers exist at $1, the price drops below peg.

This happened briefly to several stablecoins during the Terra collapse in May 2022. Even USDT temporarily dipped to $0.95 as traders rushed to exit all crypto positions. The depeg resolved as liquidity returned to normal.

Loss of Confidence:

Perhaps most dangerously, loss of confidence in a stablecoin issuer can trigger bank-run dynamics. If users believe reserves don’t exist or won’t be honored, they rush to redeem, potentially overwhelming the system.

Tether has faced persistent questions about reserve quality. During several past incidents, USDT briefly traded below $1 as confidence wavered. However, Tether has always honored redemptions, and the peg has recovered.

Technical Failures:

Smart contract bugs or oracle failures can cause crypto-backed stablecoins to depeg. If the system can’t properly value collateral or execute liquidations, the mathematical backing breaks down.

DAI briefly lost its peg during the March 2020 crypto crash when liquidations overwhelmed the system. The protocol handled the crisis, but the incident showed vulnerabilities in automated systems during extreme stress.

Can USDC or USDT Collapse Like Terra?

The short answer is: no, they can’t collapse in the same way as Terra, but they face different risks.

Terra’s collapse resulted from its fundamental design – it had no actual reserves backing UST. When confidence broke, there was nothing to stop the death spiral.

USDC and USDT hold actual reserves. If everyone tried to redeem simultaneously, the issuers could sell Treasury bills and other assets to honor redemptions. This is fundamentally different from Terra’s unbacked algorithmic design.

However, scenarios that could seriously damage USDC or USDT include:

Fraud or Mismanagement:

If Circle or Tether lied about reserves (reserves don’t exist as claimed), redemptions would fail and the stablecoin would collapse. This is why reserve transparency and audits matter so much.

Regulatory Shutdown:

Governments could potentially shut down stablecoin issuers, freeze bank accounts, or ban redemptions. This regulatory risk is real, especially for companies operating in regulatory gray areas.

Systemic Banking Crisis:

If multiple major banks failed simultaneously (a 2008-style crisis), stablecoin reserves could become trapped or impaired. The SVB incident was a small preview of this risk.

Black Swan Technical Events:

Extreme technical failures – a critical vulnerability in the blockchain protocol, issuer’s systems being hacked, etc. – could theoretically compromise stablecoin security.

While these risks exist, they’re categorically different from Terra’s design flaws. USDC and USDT have survived multiple market crashes and crises over many years, demonstrating resilience that algorithmic stablecoins couldn’t match.

Understanding Stablecoin Regulatory Risks

Regulatory uncertainty represents perhaps the biggest long-term risk to stablecoins.

Current Regulatory Landscape:

Different jurisdictions approach stablecoins very differently:

United States: Stablecoins exist in regulatory gray area. Multiple agencies claim jurisdiction (SEC, CFTC, Treasury, state regulators), creating uncertainty. Several proposed laws aim to create clear stablecoin regulations, but none have passed as of December 2025.

European Union: The Markets in Crypto-Assets (MiCA) regulation, which took effect in 2024, created comprehensive stablecoin rules. Issuers must maintain reserves, undergo audits, and comply with strict operational requirements.

United Kingdom: Following a similar path to the EU, creating a regulatory framework that treats stablecoins like electronic money institutions.

Other Jurisdictions: Approaches vary wildly. Some countries welcome stablecoins (Singapore, Switzerland), others have effectively banned them (China), and many remain uncertain.

Why Regulations Matter:

Regulations could dramatically impact stablecoin functionality:

- Reserve requirements: Mandating specific asset types could change yields and operations

- Redemption rights: Requiring issuers to honor retail redemptions would improve safety

- Banking access: Clear regulations might make it easier for issuers to maintain banking relationships

- Compliance costs: Heavy regulations could kill smaller stablecoin projects while entrenching large players

The regulatory environment continues evolving rapidly. What’s legal today might change tomorrow, creating uncertainty for both users and issuers.

Smart Contract Vulnerabilities in Crypto-Backed Stablecoins

For crypto-collateralized stablecoins like DAI, smart contract risk represents a unique vulnerability.

What Could Go Wrong:

Smart contracts are complex programs that hold billions of dollars. Bugs in this code could potentially:

- Allow unauthorized minting of stablecoins

- Enable theft of collateral

- Prevent legitimate users from withdrawing funds

- Cause incorrect liquidations

- Break the peg mechanism

The MakerDAO protocol consists of hundreds of thousands of lines of smart contract code. Despite extensive auditing and years of successful operation, the possibility of undiscovered vulnerabilities remains.

Historical Examples:

The 2020 “Black Thursday” event tested MakerDAO’s limits. During a rapid crypto crash, liquidations overwhelmed the system. Some vaults were liquidated for $0 due to a combination of network congestion and auction mechanism flaws.

The protocol survived and was subsequently improved, but the incident demonstrated how unexpected conditions can reveal vulnerabilities in even well-designed systems.

Mitigation Strategies:

- Use stablecoins that have been thoroughly audited by multiple firms

- Prefer protocols with long track records (years of operation)

- Diversify across multiple stablecoins rather than concentrating in one

- Stay informed about protocol updates and potential vulnerabilities

- Consider purchasing insurance through DeFi insurance protocols for large holdings

Bank Run Scenarios: How Likely Are They?

A bank run occurs when everyone tries to withdraw funds simultaneously, potentially overwhelming even a solvent institution.

For stablecoins, bank run dynamics work differently than traditional banks:

Fiat-Backed Stablecoins:

Circle and Tether don’t actually lend out reserves the way traditional banks do. They hold highly liquid assets (Treasury bills, cash). Therefore, they could theoretically handle large-scale redemptions if they needed to sell these assets.

However, several factors could complicate mass redemptions:

- Selling billions in Treasury bills quickly might incur losses (though likely small)

- Banking infrastructure might not process transfers fast enough

- Regulatory authorities might intervene or halt operations

- Market panic could feed on itself, with price drops causing more panic

The SVB incident demonstrated that even backed stablecoins can experience brief runs driven by fear rather than fundamental insolvency.

Crypto-Backed Stablecoins:

DAI and similar stablecoins face different bank run dynamics. Mass redemptions would require burning DAI and freeing collateral. The system is designed to handle this automatically.

However, during extreme market stress, liquidation mechanisms could become overwhelmed. If crypto collateral loses value faster than the system can liquidate positions, undercollateralization becomes possible.

MakerDAO maintains significant safety buffers and has successfully weathered multiple market crashes. Nevertheless, unprecedented market conditions could potentially stress the system beyond its limits.

Likelihood Assessment:

For established stablecoins with transparent reserves (USDC, USDT, DAI), bank runs remain unlikely under normal circumstances. These stablecoins have survived multiple crypto market crashes without failing.

However, users should understand that no stablecoin is completely immune to bank run risk. Diversifying holdings, staying informed about issuer transparency, and maintaining realistic expectations about risk are all prudent strategies.

How to Choose the Best Stablecoin for Your Needs

Different stablecoins serve different purposes. Choosing the right one depends on your specific priorities and use cases.

Best Stablecoin for Safety: USDC vs USDT

If safety is your primary concern, USDC generally represents the lower-risk choice among major stablecoins.

Why USDC Scores Higher on Safety:

Circle operates as a fully regulated U.S. company with clear compliance and transparency. Monthly reserve attestations provide regular verification of backing. Moreover, the reserve composition is simple and conservative – cash and Treasury bills only.

The company has established banking relationships with major institutions. Circle has also obtained money transmitter licenses in relevant states. This regulatory clarity reduces the risk of sudden shutdowns or legal actions.

When USDT Might Be Acceptable:

Despite less transparency, USDT has proven remarkably resilient through years of FUD (fear, uncertainty, doubt) and market stress. It has always honored redemptions, even during panic selling.

For short-term trading or situations where you need maximum liquidity, USDT’s risks may be acceptable. Many traders use USDT for active trading while keeping long-term holdings in USDC.

The Safety Hierarchy:

If I were ranking major stablecoins by safety perception:

- USDC: Highest transparency and regulatory compliance

- USDT: Large and resilient but less transparent

- DAI: Decentralized but complex with smart contract risk

- BUSD: Previously safe but being phased out (Binance focus shift)

- Algorithmic stablecoins: Highest risk, avoid unless you fully understand mechanisms

Remember that “safest” doesn’t mean completely safe. All stablecoins carry some level of risk.

Most Decentralized Option: Why Choose DAI

If decentralization and censorship resistance matter more than convenience, DAI is the clear choice.

DAI’s Decentralization Advantages:

No single company controls DAI. The entire system runs on smart contracts governed by MKR token holders. This means:

- No company can freeze your funds

- No government can shut down the issuer

- You can verify collateral backing in real-time on the blockchain

- The system continues operating even if the original creators disappeared

For users in countries with capital controls, or those philosophically committed to decentralization, these benefits outweigh DAI’s complexity and relative inefficiency.

Trade-offs to Consider:

DAI is less liquid than USDC or USDT. Fewer exchanges support it, and trading pairs are more limited. Additionally, the minimum over-collateralization creates capital inefficiency.

The system is also more complex to understand. If you don’t fully grasp how MakerDAO works, you can’t properly assess its risks.

Finally, DAI has actually become more centralized over time as the protocol accepted USDC as collateral. A significant portion of DAI is now indirectly backed by Circle’s reserves, somewhat undermining the decentralization argument.

Highest Liquidity: Which Stablecoin Is Most Available?

USDT unquestionably offers the highest liquidity and widest availability.

Liquidity Advantages:

- Available on virtually every cryptocurrency exchange globally

- Deepest order books (smallest price impact for large trades)

- Most trading pairs (you can trade almost any crypto directly for USDT)

- Fastest to move between exchanges for arbitrage

- Supported on the most blockchain networks (Ethereum, Tron, BSC, etc.)

For professional traders and market makers, USDT’s liquidity advantage often outweighs other considerations. The ability to execute large trades with minimal slippage or quickly move funds between venues is critical for their strategies.

When Liquidity Matters Most:

If you’re actively trading, need to move large amounts quickly, or operate in markets where alternatives aren’t available, USDT may be your only practical choice.

For passive holders or those making occasional transactions, liquidity matters less. USDC offers sufficient liquidity for most use cases while providing better transparency.

Inflation Hedge: When to Use PAXG (Gold-Backed)

PAXG serves a fundamentally different purpose than dollar-pegged stablecoins. Consider it when you want gold exposure with blockchain benefits.

Use PAXG When:

You want protection against dollar inflation specifically. Gold has historically maintained purchasing power across decades, unlike fiat currencies.

You want gold exposure without physical storage hassles. PAXG provides all the benefits of gold ownership without needing to secure physical bars.

You want to use gold in DeFi. Some protocols accept PAXG as collateral, enabling use cases impossible with physical gold.

You need fractional gold ownership. You can hold 0.1 PAXG (0.1 ounce of gold), which would be impractical with physical gold.

Avoid PAXG When:

You need price stability for transactions or short-term savings. PAXG fluctuates with gold prices.

You want to avoid commodity price risk. Gold can be quite volatile in the short to medium term.

You’re uncomfortable with the trust requirements. While Paxos provides attestations, you’re still trusting that physical gold exists in vaults.

The Future of Stablecoins: CBDCs, Regulation & Mass Adoption

Stablecoins stand at a fascinating crossroads between crypto innovation and traditional finance.

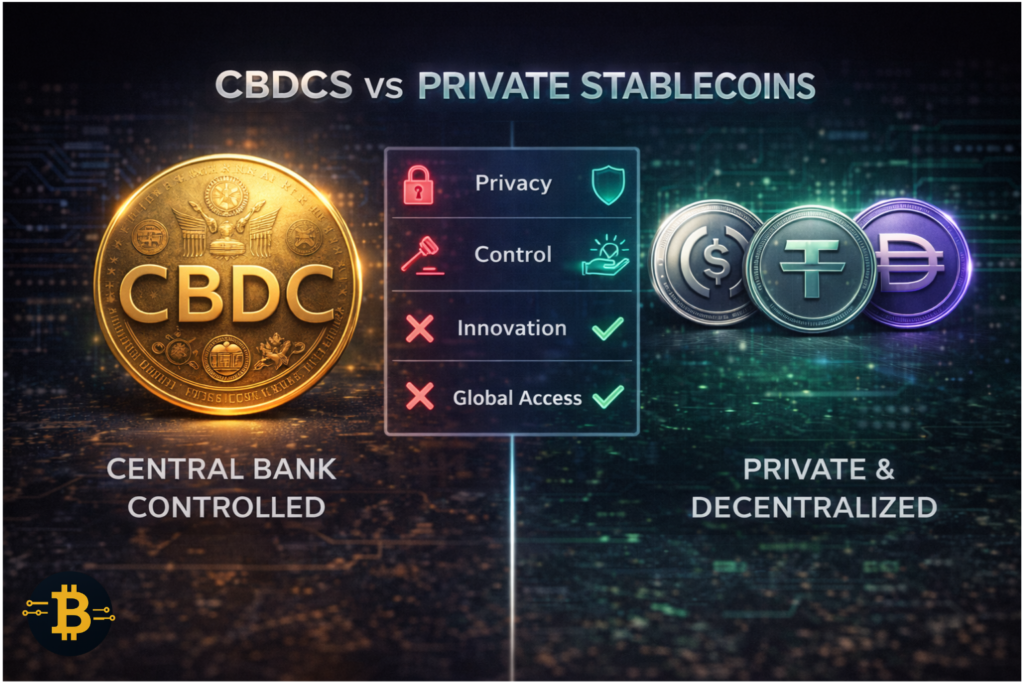

Central Bank Digital Currencies (CBDCs) vs Stablecoins

Governments worldwide are developing Central Bank Digital Currencies – essentially government-issued digital cash on blockchain-like infrastructure.

How CBDCs Differ from Stablecoins:

CBDCs represent direct claims on the central bank, just like physical cash. They’re legal tender by definition. In contrast, stablecoins are private company liabilities pegged to currency.

Central banks would have complete control over CBDC systems, including potentially seeing all transactions, setting programmable rules, and freezing accounts. Stablecoins, especially decentralized ones like DAI, offer more privacy and censorship resistance.

The Competitive Dynamic:

Some analysts predict CBDCs will kill private stablecoins. If the Federal Reserve issues a digital dollar, why use USDC?

Others argue stablecoins will remain competitive through:

- Better user experience and innovation speed

- Integration with DeFi and crypto ecosystems

- Global interoperability (CBDCs might not work across borders well)

- Privacy protections that CBDCs may lack

- Existing network effects and adoption

The reality will likely be coexistence. CBDCs may handle retail transactions and government payments, while stablecoins continue serving crypto markets, cross-border transfers, and DeFi applications.

China’s digital yuan (e-CNY) provides an early example. Despite being rolled out nationally, private cryptocurrencies and stablecoins still serve use cases the CBDC doesn’t address well.

Regulatory Framework Evolution

The next few years will bring significant regulatory clarity to stablecoins, for better or worse.

Likely Regulatory Developments:

Reserve Requirements: Regulators will probably mandate specific reserve compositions and regular audits. This should improve safety but may consolidate the market around well-capitalized issuers.

Redemption Rights: Laws may require stablecoin issuers to honor retail redemptions directly, similar to money market funds. Currently, many issuers only deal with institutional partners.

Banking Integration: Clear regulations could help stablecoin issuers maintain banking relationships more easily. Conversely, regulations might require stablecoins to become actual banks, dramatically increasing compliance costs.

Cross-Border Coordination: International standards will likely emerge, similar to banking regulations. The Financial Stability Board and other international bodies are actively working on stablecoin frameworks.

Consumer Protections: Expect regulations requiring clear disclosures about risks, reserve backing, and the fact that stablecoins aren’t FDIC-insured.

Impact on Different Stablecoin Types:

Fiat-backed stablecoins from regulated companies like USDC will likely thrive under clear regulations. They’re already operating in a quasi-regulated manner.

Decentralized stablecoins like DAI face uncertain treatment. How do you regulate a protocol with no central operator? Some jurisdictions may struggle to fit them into existing frameworks.

Algorithmic stablecoins may face outright bans or extremely restrictive requirements following the Terra collapse. Regulators view them as inherently unstable.

Path to Mainstream Adoption

For stablecoins to achieve true mainstream adoption, several barriers must fall:

User Experience: Current stablecoin usage requires understanding wallets, blockchain addresses, gas fees, and other crypto-native concepts. Mass adoption requires interfaces as simple as Venmo or PayPal.

Merchant Acceptance: More businesses need to accept stablecoin payments directly. This requires better point-of-sale systems and accounting integration.

Regulatory Clarity: Businesses won’t fully commit to stablecoins until they understand the legal framework. Clarity will unlock corporate adoption.

Banking Integration: Easier on-ramps and off-ramps between traditional banking and stablecoins would dramatically improve usability.

Education: Most people still don’t understand what stablecoins are or why they’d use them. Widespread adoption requires better education about benefits and risks.

Scaling Solutions: Transaction costs must remain low even during network congestion. Layer 2 solutions and more efficient blockchains are helping here.

Trust Building: More time without major collapses will gradually build confidence. The Terra collapse set back mainstream acceptance significantly.

Despite these challenges, stablecoin adoption is growing rapidly. Transaction volume exceeds $10 trillion annually. Countries with unstable currencies increasingly rely on them. Major payment companies are launching their own stablecoins.

The trajectory suggests stablecoins will become standard financial infrastructure within the next 5-10 years, though probably not replacing traditional currency entirely.

Are Stablecoins Safe? Common Questions Answered

Let’s address the most frequent questions about stablecoin safety and usage.

What happens if a stablecoin issuer goes bankrupt?

This depends on how assets are held and which legal framework applies.

For USDC, Circle maintains reserves in custody accounts specifically designated for USDC holders. These accounts should be bankruptcy remote, meaning Circle’s creditors couldn’t claim them if the company failed. Nevertheless, the actual legal treatment would depend on court proceedings and precedent that doesn’t fully exist yet.

For USDT, the legal structure is more complex because Tether operates offshore. How reserves would be treated in bankruptcy isn’t entirely clear.

For DAI, bankruptcy isn’t relevant because there’s no company. The protocol holds all collateral in smart contracts. If the MakerDAO organization ceased to exist, the protocol would continue operating automatically.

This uncertainty is why diversification across multiple stablecoins can be prudent for large holdings.

How do stablecoins compare to traditional savings accounts?

Stablecoins and savings accounts serve different purposes with different risk profiles.

Advantages of Stablecoins:

- Higher yields available through DeFi (though with significantly higher risk)

- Instant global transfers 24/7

- No minimum balance requirements

- Permissionless access (no bank approval needed)

- Potential for anonymity/privacy

Advantages of Traditional Savings:

- FDIC insurance up to $250,000

- Established legal protections

- Simpler for tax purposes

- Easier integration with bill pay and other banking

- Generally more trusted by non-crypto users

For most people, traditional savings accounts should anchor emergency funds and short-term savings due to FDIC insurance. Stablecoins can complement this for specific use cases like earning higher yields on risk capital, making international transfers, or accessing DeFi.

Can stablecoins be frozen or seized?

Yes, most fiat-backed stablecoins can be frozen by their issuers.

Both Circle and Tether comply with law enforcement requests and can freeze addresses associated with illegal activity. They’ve done this for addresses linked to hacking, fraud, and other crimes.

From a civil liberties perspective, this is controversial. Proponents argue it’s necessary for regulatory compliance and preventing criminal misuse. Critics view it as undermining crypto’s censorship resistance.

Interestingly, stablecoins have occasionally frozen funds incorrectly. In some cases, innocent users had funds frozen due to receiving transfers from problematic addresses. These situations usually get resolved but can cause temporary hardship.

DAI cannot be frozen the same way because there’s no central entity controlling the protocol. However, the protocol can blacklist addresses from certain functions, and MKR holders could theoretically vote to upgrade the protocol with freezing capabilities.

What’s the tax treatment of stablecoins?

Tax treatment varies by jurisdiction and continues evolving. In the United States:

Trading between cryptocurrencies (including stablecoins) typically triggers capital gains or losses. Exchanging Bitcoin for USDC is a taxable event, not just converting USDC back to dollars.

However, converting between similar stablecoins (like USDC to USDT) may qualify for like-kind exchange treatment in some interpretations, though this is uncertain and risky to rely on.

Interest earned on stablecoins is treated as ordinary income, similar to bank interest. This includes DeFi yields.

The IRS hasn’t provided completely clear guidance on all stablecoin scenarios. Working with tax professionals familiar with crypto is strongly recommended.

Other countries have different approaches. Some treat stablecoins like regular currency for tax purposes, while others apply capital gains treatment to every transaction.

Should I hold all my money in stablecoins?

Absolutely not, for several reasons:

First, stablecoins aren’t FDIC insured. Your traditional bank account protects up to $250,000 through federal insurance. Stablecoins have no equivalent protection.

Second, regulatory uncertainty remains significant. Rules could change in ways that affect access to your funds or how they can be used.

Third, even the safest stablecoins carry risks that traditional bank accounts don’t – smart contract risk, issuer bankruptcy risk, blockchain network failures, etc.

Fourth, tax treatment can be more complex, creating accounting headaches.

Stablecoins make sense as part of a broader financial strategy – for specific use cases like international transfers, DeFi participation, or crypto trading. However, they shouldn’t replace traditional banking for your emergency fund or essential savings.

A reasonable approach might be:

- 80-90% in traditional FDIC-insured accounts

- 10-20% in stablecoins for crypto activities and experimenting with DeFi

- Even less if you’re highly risk-averse or unfamiliar with crypto

Always assess your own risk tolerance and financial situation rather than following generic advice.

Do stablecoins work during internet outages?

No, stablecoins require internet connectivity to transact. They exist entirely on digital blockchain networks, so you need online access to send, receive, or verify balances.

This represents a genuine limitation compared to physical cash, which works during any infrastructure failure. For this reason, maintaining some physical currency for emergencies remains wise, especially in areas prone to natural disasters or infrastructure problems.

However, once internet connectivity resumes, stablecoins work normally. The blockchain doesn’t forget transactions or lose data during outages – it simply pauses until nodes can communicate again.

Some projects are exploring offline crypto transactions through technologies like mesh networks or satellite connectivity, but these remain experimental.

Which stablecoin is best for beginners?

USDC represents the best starting point for most crypto beginners.

Circle’s regulatory compliance, transparent monthly attestations, and simple reserve structure make it easier to understand than alternatives. Additionally, major exchanges and wallets prominently support USDC, simplifying the onboarding process.

The company also provides better customer support channels than decentralized alternatives, which matters when you’re learning. Moreover, institutions and mainstream financial companies increasingly integrate USDC, suggesting long-term staying power.

Start with small amounts while learning. Buy $50-100 of USDC, practice sending it between wallets, and explore basic DeFi applications before committing significant funds.

How quickly can I convert stablecoins back to regular money?

This depends on your chosen method and location.

Through Exchanges: Most centralized exchanges process stablecoin-to-fiat withdrawals within 1-3 business days. You sell USDC for USD on the exchange, then withdraw to your linked bank account.

Coinbase, for instance, typically processes ACH bank transfers in 1-2 business days for U.S. customers. Wire transfers are faster (same day to next day) but cost more.

Direct Redemption: If you qualify for direct redemption with Circle (typically requires minimum amounts of $100,000+), conversions happen within one business day.

Peer-to-Peer: In some countries, peer-to-peer exchanges enable nearly instant conversions. You sell stablecoins directly to other users who pay via local payment methods.

Geographic Variations: Conversion speed varies dramatically by country. Developed markets with strong banking infrastructure offer faster service. Emerging markets may have fewer options and longer delays.

The fastest path is maintaining accounts on major exchanges in advance, with banking information already verified. This eliminates setup delays when you need to convert quickly.

Final Thoughts: Using Stablecoins Wisely in 2025

After ten years of teaching cryptocurrency concepts, I’ve watched stablecoins evolve from niche experiments to essential financial infrastructure. They now facilitate trillions of dollars in annual transactions, provide financial access to millions in unstable economies, and underpin the entire DeFi ecosystem.

However, stablecoins aren’t magic internet money without risk. The Terra/UST collapse vividly demonstrated that clever mechanisms can fail catastrophically. Even established stablecoins carry risks ranging from regulatory uncertainty to bank failures.

The key to using stablecoins safely involves:

Understanding what backs them. Never use a stablecoin without knowing its reserve composition and verification methods. If you can’t explain how it maintains its peg, you don’t understand it well enough to trust it with significant funds.

Diversifying across types. Don’t concentrate all holdings in a single stablecoin. Consider holding both USDC and DAI, for example, to balance centralization risks differently.

Staying informed about risks. Follow news about your chosen stablecoins, regulatory developments, and reserve attestations. The landscape changes quickly.

Using established options. Stick with stablecoins that have survived multiple market cycles. Consequently, avoid new projects promising revolutionary mechanisms—we’ve seen how those stories end.

Maintaining realistic expectations. Stablecoins aren’t FDIC-insured bank deposits. They’re experimental financial instruments that happen to work well most of the time. Therefore, treat them accordingly in your risk management.

Looking forward, stablecoins will likely become even more integrated into global finance. Regulatory clarity will emerge, making them safer and more accessible. Major technology and financial companies will continue launching stablecoins. CBDCs will coexist with private options rather than replacing them entirely.

For individuals, stablecoins offer genuine benefits: cheaper international transfers, access to stable currency regardless of location, and participation in the emerging DeFi economy. These benefits will expand as technology improves and regulations clarify.

Start small if you’re new to stablecoins. Buy a small amount of USDC, send it between wallets, and explore basic applications. Gradually increase involvement as your understanding deepens.

The technology works. Just use it wisely, understand the risks, and never invest more than you can afford to lose.

About This Guide

This comprehensive guide was researched using data from official stablecoin issuer documentation, blockchain analytics platforms, regulatory filings, and established financial institutions. All market capitalization figures, reserve compositions, and regulatory information are current as of December 2025.

Last Updated: December 27, 2025

Primary Sources

Information about stablecoin mechanisms, reserve structures, and operational details comes from official documentation including Circle’s transparency reports, Tether’s attestations, MakerDAO’s technical documentation, and public blockchain data. Historical data regarding the Terra/UST collapse is sourced from blockchain explorers, contemporary reporting, and post-mortem analyses from blockchain security firms.

Regulatory Information: Details about stablecoin regulations, including the EU’s MiCA framework and U.S. regulatory developments, are sourced from official government documents, the Financial Stability Board, and regulatory agency announcements.

Market Data: Stablecoin market capitalizations, trading volumes, and pricing information are aggregated from CoinGecko, CoinMarketCap, and blockchain analytics platforms that track on-chain data in real-time.

Technical Documentation: Smart contract mechanisms for crypto-collateralized stablecoins are explained based on official protocol documentation from MakerDAO, Ethereum.org, and audited smart contract code available on public blockchains.

Important Disclaimer: This content is strictly educational and does not constitute financial, investment, or legal advice. Stablecoins involve significant risks including potential depeg events, regulatory changes, smart contract vulnerabilities, issuer bankruptcy, and complete loss of funds. The Terra/UST collapse in May 2022, which destroyed $40 billion in value, demonstrates that even large, popular stablecoins can fail catastrophically. Past performance does not guarantee future results. Always conduct thorough independent research, understand all risks involved, and consider consulting with qualified financial, legal, and tax advisors before using stablecoins or engaging in cryptocurrency transactions. Never invest or use more capital than you can afford to lose completely.

References

An Unbiased Global Financial System. (n.d.). Makerdao.com. Retrieved December 27, 2025, from https://makerdao.com/

MakerDAO technical docs. (n.d.). Makerdao.com. Retrieved December 27, 2025, from https://docs.makerdao.com/

Markets in crypto-Assets Regulation (MiCA). (n.d.). Europa.Eu. Retrieved December 27, 2025, from https://www.esma.europa.eu/esmas-activities/digital-finance-and-innovation/markets-crypto-assets-regulation-mica

Pax gold (PAXG). (n.d.). Paxos.com. Retrieved December 27, 2025, from https://paxos.com/paxgold/

Powering global finance. Issued by Circle. (n.d.). Circle.com. Retrieved December 27, 2025, from https://www.circle.com/en/usdc

PYUSD Stablecoin. (n.d.). Paypal.com; PayPal. Retrieved December 27, 2025, from https://www.paypal.com/us/digital-wallet/manage-money/crypto/pyusd

Stablecoins. (n.d.). Ethereum.org; Ethereum Foundation. Retrieved December 27, 2025, from https://ethereum.org/en/stablecoins/

Tether – official home of Tether. (n.d.). Tether.To. Retrieved December 27, 2025, from https://tether.to/en/transparency/

Tether – official home of tether. (n.d.). Tether.To. Retrieved December 27, 2025, from https://tether.to/

Top Stablecoin tokens by market capitalization. (n.d.). CoinMarketCap. Retrieved December 27, 2025, from https://coinmarketcap.com/view/stablecoin/

What is cryptocurrency? Beginner’s guide 2025. (2025, October 7). Cryptogiant –. https://cryptogiant.io/what-is-cryptocurrency/

(N.d.-a). Coingecko.com. Retrieved December 27, 2025, from https://www.coingecko.com/en/categories/stablecoins

(N.d.-b). Circle.com. Retrieved December 27, 2025, from https://www.circle.com/en/usdc/transparency

(N.d.-c). Coinbase.com. Retrieved December 27, 2025, from https://www.coinbase.com/